El primer ETF que compré no fue porque fuera, el mejor. Fue porque sonaba impresionante y a todos en línea parecía encantarles. Así suelen empezar los errores.

Choosing the right ETF isn’t about finding the hottest ticker or the one with the flashiest theme. It’s about understanding what role that ETF plays inside your portfolio. When I stopped asking “Which ETF is best?” and started asking “Best for what?” my decisions improved immediately.

There are more than 3,000 ETFs listed in the U.S. alone, covering everything from total market exposure to robotics, uranium mining, frontier markets, and leveraged volatility bets. According to the Investment Company Institute (ICI), U.S. ETFs held approximately $13.37 trillion in assets as of December 2025.

ICI data: https://www.ici.org/research/stats/etf/etfs_12_25

That scale is impressive. But it also means choice overload. So here’s how I personally narrow it down.

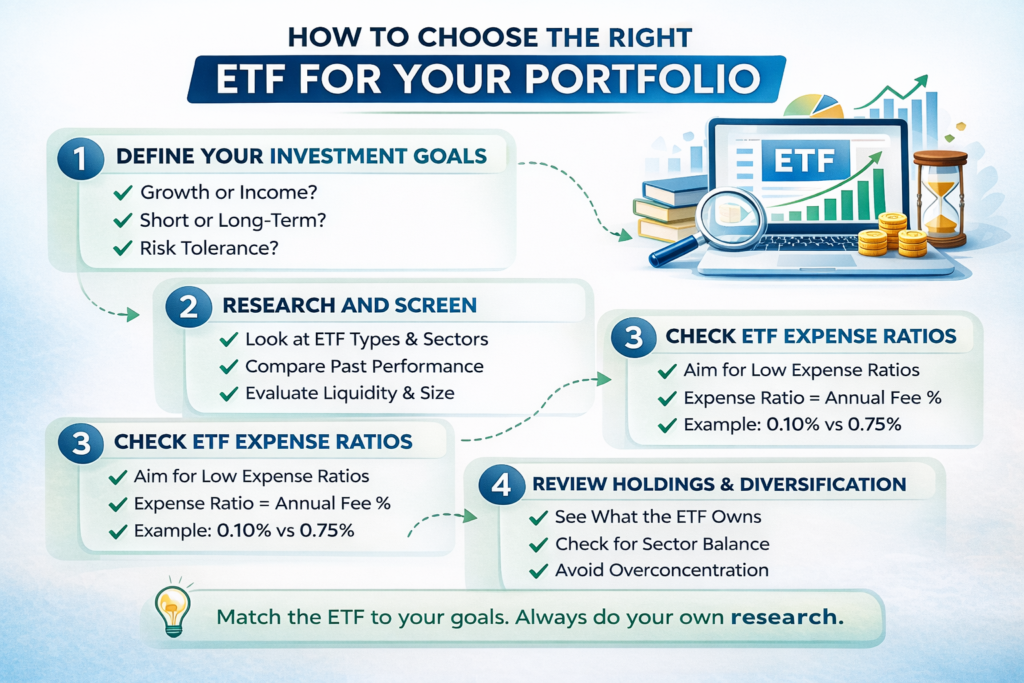

Step One: Define the Job of the ETF

Before I even look at a ticker, I decide what I need.

Is this ETF supposed to:

- Anchor my portfolio?

- Add diversification?

- Increase growth potential?

- Provide income?

- Hedge risk?

If I don’t define the job first, I end up buying overlap or taking unintended risk.

For example, if I already own a total U.S. market ETF and then buy a large-cap growth ETF because it’s trending, I might just be doubling down on the same mega-cap stocks without realizing it.

The U.S. stock market itself is already concentrated. In recent years, the top 10 companies in the S&P 500 have represented around 30% or more of the index’s total weight. That concentration affects diversification whether you notice it or not.

Step Two: Understand What the ETF Actually Holds

Names can be misleading. “Global opportunity innovation future disruption ETF” tells me nothing useful.

I check:

- Top 10 holdings

- Sector allocation

- Geographic exposure

- Number of holdings

- Market cap breakdown

The SEC explains that ETFs are required to disclose holdings regularly, and most major providers publish them daily.

SEC investor bulletin: https://www.sec.gov/investor/alerts/etfs.pdf

If an ETF claims diversification but 45% of assets sit in five stocks, that’s not broad exposure. That’s concentrated exposure wearing a diversification costume.

Step Three: Expense Ratio (Because Fees Compound)

Fees aren’t exciting, but they’re predictable.

Según el informe de ICI de 2024, el ratio de gastos promedio ponderado por activos para los ETF de acciones indexadas fue del 0,14% , y para los ETF de bonos indexados fue del 0,10% .

Datos de comisiones de ICI: https://www.ici.org/files/2025/per31-01.pdf

That’s what investors actually pay on average.

If I’m choosing between two nearly identical S&P 500 ETFs and one costs 0.03% while the other costs 0.50%, I need a very strong reason to justify paying more.

A 0.40% fee difference on a $300,000 portfolio is $1,200 per year. Over 20 years, that’s not just $24,000. It’s the growth of that $24,000 that you also lose.

Low cost doesn’t guarantee high returns. But high cost guarantees less return.

Step Four: Liquidity and Trading Costs

Expense ratio is only part of cost.

I also look at:

–Volumen promedio diario de operaciones

–Diferencial entre oferta y demanda

–Activos bajo gestión (AUM)

FINRA explains that ETF investors should pay attention to liquidity and spreads because they impact execution price.

FINRA overview: https://www.finra.org/investors/investing/investment-products/exchange-traded-funds-and-products

A niche ETF might have a low expense ratio but wide spreads. That can cost more than the annual fee if you trade carelessly.

For large core holdings, I prefer ETFs with substantial AUM and tight spreads. Not because small funds are “bad,” but because liquidity reduces friction.

Step Five: Index Methodology Matters More Than the Brand

Two ETFs can track different indexes and both claim to represent “the total market.”

Some indexes are market-cap weighted. Others use equal weighting, factor tilts, or screening criteria. For example:

Market-cap weighting gives more weight to larger companies.

Equal-weighted indexes rebalance regularly and can tilt toward smaller companies.

Factor-based ETFs might tilt toward value, quality, or momentum.

Those differences create meaningful performance variation over time.

I don’t just read the marketing summary. I look at the index methodology document. It sounds boring, but it tells me exactly what I’m buying.

Step Six: Know the Risk Profile

Historical volatility is not a guarantee of future results, but it gives context.

Broad U.S. equities have historically delivered around 9–10% average annual returns over long periods, but with significant drawdowns exceeding 30% in severe bear markets.

Bond ETFs have lower expected returns but are sensitive to interest rates. In 2022, many long-duration bond ETFs declined significantly due to rising rates.

If I can’t tolerate a 20–30% decline, I shouldn’t be buying 100% equity ETFs and hoping for emotional strength later.

Choosing the right ETF is partly about choosing the right level of volatility for your psychology.

Step Seven: Avoid Overlap

This one is sneaky.

I once held three ETFs thinking I was diversified:

- Total U.S. market

- Large-cap growth

- Tech innovation

When I mapped the holdings, I realized I was massively overweight the same handful of mega-cap tech companies.

Diversification isn’t about the number of ETFs. It’s about exposure differences.

Morningstar and other platforms allow you to see portfolio overlap. Even manually checking top holdings can reveal redundancy.

Step Eight: Understand Tax Efficiency

One of the structural advantages of ETFs is their in-kind creation and redemption process, which can reduce capital gains distributions compared to mutual funds.

The SEC and multiple providers explain that ETFs often distribute fewer capital gains because of this structure.

SEC overview: https://www.sec.gov/investor/pubs/sec-guide-to-mutual-funds.pdf

For taxable accounts, this matters.

Tax efficiency isn’t the headline feature people talk about, but over decades it can improve after-tax returns meaningfully.

Step Nine: Decide Core vs Satellite

I personally divide ETFs into two categories:

Core holdings are broad, low-cost, long-term positions. Think total market, S&P 500, aggregate bond exposure.

Satellite positions are smaller allocations that express a specific view. Maybe emerging markets, small caps, or a thematic bet.

If I treat everything like a satellite, my portfolio becomes chaotic. If everything is core, I may lack flexibility.

Most long-term portfolios are built around a small number of broad ETFs.

Step Ten: Simplicity Usually Wins

There’s a psychological trap where complexity feels intelligent.

But the data on investor behavior suggests that simplicity often produces better outcomes because it’s easier to stick with during downturns.

According to ICI and other long-term studies, investors tend to underperform the funds they invest in due to timing decisions. Complexity increases the temptation to tinker.

Choosing the right ETF is not about maximizing cleverness. It’s about maximizing the probability that you’ll stay invested.

My Personal Filter

When I choose an ETF, I ask:

What job does it serve?

Is the exposure clear and intentional?

Is the cost reasonable compared to similar alternatives?

Is liquidity solid?

Does it meaningfully improve diversification?

Si pasa esas pruebas, se gana un lugar.

Si no es así, no lo compro sólo porque esté de moda.

Ejemplos de ETFs según objetivo:

Final Thoughts

There is no universally “best” ETF. There is only the ETF that fits your allocation, your time horizon, and your risk tolerance.

Broad, low-cost index ETFs are often the backbone of successful long-term portfolios because they are simple, transparent, and cost-efficient.

But the right ETF for a 25-year-old with a 30-year horizon is not necessarily the right ETF for someone approaching retirement.

Choosing wisely is less about prediction and more about alignment.

And alignment beats hype every time.

This site was built to simplify ETF investing and remove the noise. You can read more about our approach and principles on the About page.

Leave a Reply