When I first started investing in ETFs, I thought taxes would be simple — like just paying a small fee when I sold something. I quickly learned taxes are one of those things that sound straightforward… until you actually look at the numbers, the IRS rules, and the fine print. Let’s break this down in a real, practical way so you actually understand how ETFs are taxed in the U.S. without the confusion.

What Is an ETF? A Quick Reminder

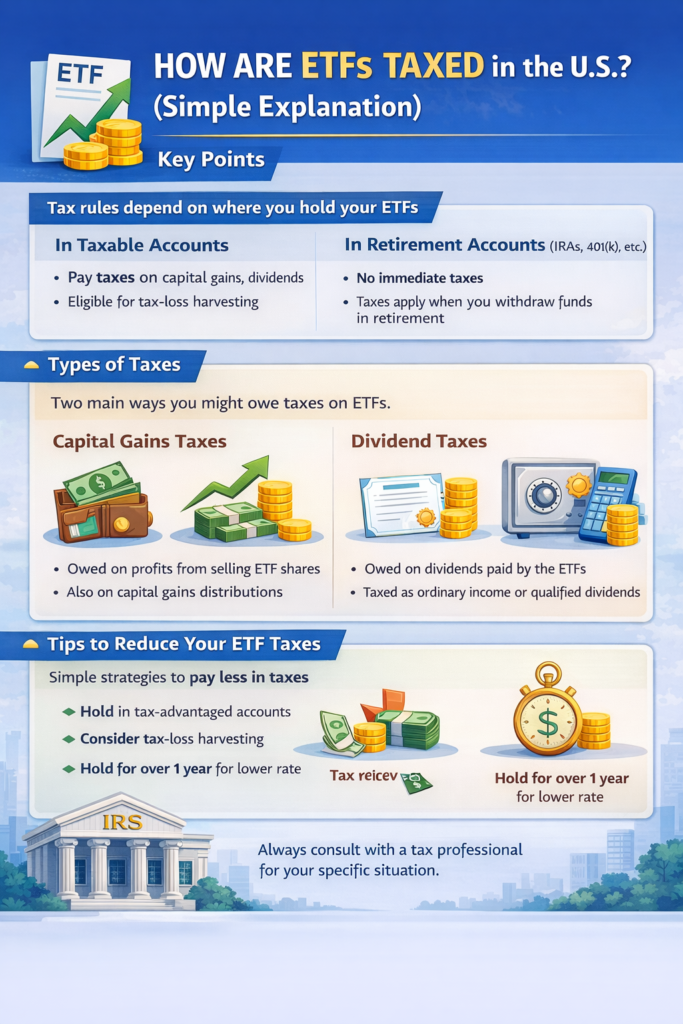

An ETF (exchange-traded fund) is basically a basket of assets — stocks, bonds, commodities — that trades on an exchange just like a stock. The IRS taxes ETFs much like it taxes individual stocks and mutual funds, but a few quirks make ETFs more tax-efficient than mutual funds.

1. Taxes You Pay When You Sell ETF Shares

The first big way ETFs are taxed is when you sell them for a profit — what the IRS calls a capital gain.

Short-Term vs. Long-Term Capital Gains

How long you hold the ETF matters.

- Short-term capital gains – If you hold an ETF for one year or less, the profit is taxed at your ordinary income tax rate — which today can be anywhere from about 10% up to 37% depending on your income and filing status.

- Long-term capital gains – If you hold the ETF more than one year, you pay the favorable long-term capital gains rates, which in 2025–2026 are 0%, 15%, or 20% depending on your taxable income.

For example, if I sold an ETF I owned for two years and my taxable income was in the middle range, I’d likely pay 15% on those gains instead of my regular income tax rate.

This is the main tax most investors think of.

2. ETF Dividends and How They’re Taxed

Many ETFs distribute dividends if they hold dividend-paying stocks or interest if they hold bonds.

Those distributions are reported to you on Form 1099-DIV, and the IRS treats them in two main ways:

Qualified Dividends

If the dividends meet specific IRS requirements, they’re taxed at the lower long-term capital gains rates (0%, 15%, or 20%) — the same rates you’d pay on long-term capital gains.

To qualify, you usually have to have held the ETF long enough around the dividend date.

Non-Qualified (Ordinary) Dividends

If they don’t meet the criteria, dividends are taxed at your normal income tax rate, which for many people is higher than the capital gains rate — sometimes up to 37%.

This matters especially with ETFs that hold special assets like REITs or certain foreign stocks — they often pay ordinary dividends.

3. Capital Gains Distributions From the Fund

One advantage of ETFs over mutual funds is that ETFs typically distribute very few capital gains to shareholders.

Mutual funds often sell stocks inside the fund to meet redemptions, and that forces the fund to pass capital gains on to all investors — sometimes every year.

ETFs use an “in-kind redemption mechanism” where authorized participants exchange securities rather than cash, so the fund doesn’t have to sell assets as much. This significantly reduces taxable capital gains distributions.

According to industry data, only a small percentage of ETFs distribute capital gains in a given year compared to a much higher percentage of mutual funds.

In practical terms, this means if I hold a broad-market ETF inside a taxable brokerage account, I probably won’t see unexpected capital gains hits very often — which is nice.

4. The Net Investment Income Tax (NIIT)

There’s another tax that many people don’t think about right away: the Net Investment Income Tax (NIIT).

If your modified adjusted gross income (MAGI) is above certain thresholds — roughly $200,000 for single filers or $250,000 for married filing jointly — you might owe an additional 3.8% tax on investment income, including capital gains and dividends.

This tax is on top of your normal federal taxes, so high-income investors should definitely factor it in when estimating their tax bill on ETF profits and income.

5. State and Local Taxes

Most of the time we talk about federal taxes, but many states also tax your investment gains and dividend income. States like California and New York treat capital gains as ordinary income.

If you live in a state with no income tax — like Florida or Texas — you might avoid state tax on your ETF profits entirely.

Always check your own state’s tax rules — these vary widely.

A Real Example

Let’s say I bought 100 shares of an ETF at $100/share ($10,000 total). Over three years, it grows to $150/share, so my investment is now worth $15,000.

- If I sell, my long-term capital gain is $5,000.

• If I’m in the 15% long-term capital gains bracket, I owe $750 in federal tax.

• If I also owe the 3.8% NIIT, that’s another $190.

So my total bill on that gain might be around $940 — not trivial, but much lower than if it were all ordinary income.

Now let’s assume it paid dividends of $200 over that time. If these were qualified dividends, I might pay the 15% rate on that too. If they were ordinary, I could be paying my full income tax rate.

This is why holding periods and dividend classifications matter.

6. ETFs in Tax-Advantaged Accounts

One of the simplest ways to deal with ETF taxes is to hold them in a tax-advantaged account like a Traditional IRA, Roth IRA, or 401(k).

- In a Roth IRA, qualified withdrawals are tax-free in retirement.

- In a Traditional IRA/401(k), you defer taxes until you take money out.

If I know I’m using an ETF for long-term retirement savings, I usually put it in these accounts to avoid most taxes while the money is working.

7. Foreign ETFs and Withholding Taxes

If an ETF holds foreign stocks, you might face foreign withholding taxes on dividends before you even receive them. Some ETFs are structured to reclaim these taxes for U.S. investors, but rules vary.

This is more advanced, and you’ll want to look at the ETF’s prospectus to understand how foreign taxes are treated.

8. Tax Forms You’ll Receive

In most years you’ll get:

- Form 1099-DIV — for dividend income and capital gains distributions.

- Form 1099-B — when you sell ETF shares, reporting your cost basis and proceeds.

I always keep these forms organized because they’re what I use to fill out my tax return or give to my accountant.

9. Tax Planning Tips (From My Experience)

There are a few practical things that helped me keep more of what I earned:

✔ Aim for long-term holding — at least a year — to benefit from lower capital gains rates.

✔ Use tax-advantaged accounts for ETFs that pay big dividends.

✔ Harvest losses — if some ETFs lost value, consider selling them to offset gains.

✔ Consider your income level — if you’re near the threshold for the NIIT, talk with a tax professional.

These are not strict rules, but simple habits that can make a noticeable difference at tax time.

Conclusion

ETFs aren’t magically tax-free, but they are generally more tax-efficient than mutual funds because of how they’re structured. You’ll pay taxes on dividends and on profits when you sell, and the rates depend on how long you hold and your income level.

Getting comfortable with how these taxes work gives you a real edge because taxes eat into your returns every year.

If you want official IRS guidance on how dividends and capital gains are taxed, check out IRS Topic No. 404 (Dividends) at the IRS website.

Tax rules change often, and everyone’s situation is a bit different. When in doubt, talk to a qualified tax advisor.

This site was built to simplify ETF investing and remove the noise. You can read more about our approach and principles on the About page.

Leave a Reply