The first time I bought an ETF, I remember thinking the “expense ratio” was basically trivia. A tiny percentage printed on a fact sheet, something you glance at once and never worry about again. Then I did the math over a long time horizon and realized this is one of those boring details that quietly decides whether you end up with “nice gains” or “why is my portfolio smaller than it should be?”

An expense ratio is not a one-time fee. It’s a cost you pay every year you own the fund. You don’t get an invoice, and you don’t see a charge hit your brokerage account. Instead, it’s deducted internally from the fund’s assets, which slightly reduces your return over time. The SEC describes an expense ratio as a fund’s total annual operating expenses expressed as a percentage of average net assets, including management fees and other expenses.

So what exactly are you paying for, how big is it really, and when does it matter enough to change what you buy?

What an expense ratio is (in plain English)

The expense ratio is the annual percentage of your investment that goes to running the ETF. Think of it as the “operating cost” of the fund: portfolio management, administration, recordkeeping, custody, legal and accounting work, and sometimes marketing and distribution. Vanguard explains it simply as the cost of portfolio management, administration, marketing, and distribution, deducted from returns before you get them.

If an ETF has a 0.10% expense ratio, that means you pay about $1 per year for every $1,000 invested. If it’s 0.03%, you pay about $0.30 per year per $1,000. That sounds laughably small until you apply it to a large balance for decades.

How it’s collected (and why you don’t “see” it)

You’re not paying the fee as a separate debit. The ETF reduces its net asset value slightly as it accrues expenses. That’s why it feels invisible. The cost is real, it’s just baked into performance.

This matters because people underestimate invisible costs. Humans will spend 20 minutes hunting for a $5 coupon and then ignore a fee that quietly compounds into thousands of dollars.

What’s usually inside the expense ratio (and what usually isn’t)

The expense ratio generally covers the ongoing costs to operate the fund. The SEC also notes that a fund’s expense ratio typically does not include trading costs inside the portfolio (like brokerage commissions when the fund buys and sells holdings).

That leads to a useful point: the expense ratio is important, but it’s not the only cost. Turnover, spreads, and taxes can matter too, depending on the ETF.

“What’s a good expense ratio?” depends on the ETF type

In broad U.S. index ETFs, fees have been crushed by competition. The Investment Company Institute (ICI) reported that in 2024, the asset-weighted average expense ratio for index equity ETFs was 0.14%, and for index bond ETFs it was 0.10%.

Two things jump out at me from that:

First, 0.14% is already pretty low as an “average investors actually pay” measure. Second, it’s an asset-weighted average, meaning it reflects where real money sits, not just the existence of a bunch of overpriced niche funds. That’s why the “simple average” you sometimes see quoted can be higher, because it gives tiny expensive ETFs the same weight as huge cheap ones.

Now, if you’re buying a specialized ETF, the “good” number changes. Emerging markets small-cap, high-yield credit, active strategies, thematic ETFs, alternatives, and anything using complicated derivatives often costs more. Higher fees aren’t automatically evil, but they need to earn their keep.

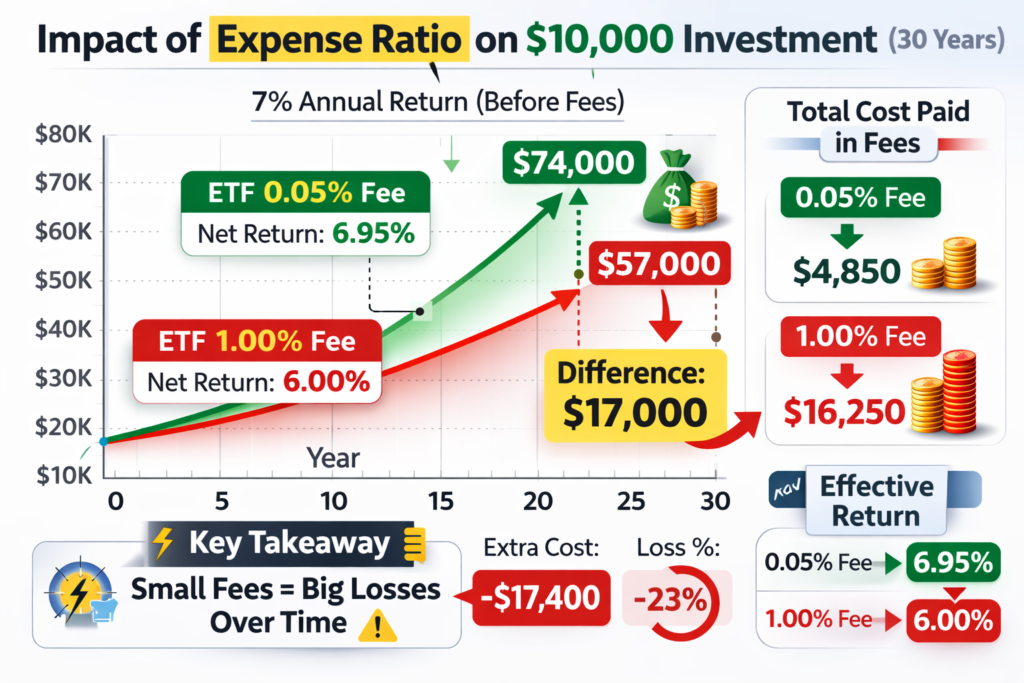

The math that makes expense ratios matter

Let’s put numbers on it, because numbers are the only thing finance people respect.

Assume you invest $10,000 and hold it for 30 years. Also assume the market gives you an average 7% annual return before fees (just a hypothetical). Compare two ETFs that hold basically the same type of assets:

- ETF A: 0.03% expense ratio

- ETF B: 0.50% expense ratio

That fee difference is 0.47% per year. It doesn’t sound dramatic. Over 30 years, it’s not “0.47%.” It’s the compounding you lose.

Even a large provider like State Street illustrates the intuition with a simple example: $10,000 in an ETF with a 0.04% expense ratio costs about $4 in a year (roughly, depending on changes in value).

Now scale that to a real life portfolio. A difference of 0.40% on a $200,000 balance is about $800 per year. Over decades, it snowballs, because the money you pay in fees isn’t invested anymore. You lose not only the fee but also the future growth of that fee.

This is why “low cost” became almost a religion in long-term indexing circles. Not because fees are the only factor, but because fees are one of the few factors you can control with certainty.

When expense ratios matter a lot (and when they matter less)

Expense ratios matter most when three things are true: you’re holding long term, the ETF exposure is commoditized (meaning many funds offer basically the same thing), and the fee gap is meaningful.

If I’m buying a plain S&P 500 ETF or a total market ETF, the underlying exposure is not unique. There are multiple funds that track essentially the same benchmark and charge 0.03% or less in some cases, as Fidelity notes when discussing S&P 500 ETF pricing.

In that situation, paying 0.70% for a “thematic innovation mega disruption future” ETF that mostly ends up holding the same large-cap tech names is hard for me to justify.

On the other hand, expense ratios matter less if the ETF provides something genuinely hard to access cheaply. Certain bond segments, actively managed fixed income, or niche exposures might cost more, but if they deliver what I need, the fee can be acceptable. The key is that I want a reason other than marketing.

Expense ratio vs other costs you should not ignore

An ETF’s expense ratio is only one line item. Trading costs can be just as relevant in the real world.

If an ETF has a wide bid-ask spread, you can lose more in one sloppy market order than you’ll pay in fees all year. Also, some ETFs have “acquired fund fees and expenses” when they hold other funds, which can raise costs in ways people don’t notice. Charles Schwab highlights that fund-of-funds structures can have higher expense ratios partly for this reason.

For long-term investors, my personal rule is simple: start with expense ratio, then sanity-check spreads, turnover, and what the ETF actually holds. A low fee doesn’t fix a bad product.

Where to find the expense ratio (and what to watch for)

You can find an ETF’s expense ratio on the fund sponsor’s page, the prospectus fee table, and most broker research pages. Investor.gov points out that fund fees and expenses are listed in a standardized fee table near the front of the prospectus.

Two quick warnings I keep in mind:

One, some ETFs advertise a low “gross” fee but have waivers that make the “net” fee lower temporarily. Waivers can expire. I prefer to know what the fund will cost when the training wheels come off.

Two, make sure you’re comparing apples to apples. Some products are ETFs, some are ETNs, some are commodity pools. The fee line might not tell the full story, and the risk structure can be different.

The big picture: fees have fallen, and that’s good for you

The trend is your friend here. ICI’s 2024 data shows expense ratios have continued to decline, especially for index funds and index ETFs, because investors keep moving money into cheaper options.

This doesn’t mean every cheapest ETF is automatically “best.” It means the baseline is now low enough that you should demand a clear benefit before paying materially more.

My bottom line

If I’m investing for the long run in a broad, commoditized asset class, I treat the expense ratio like a non-negotiable filter. It’s not the only thing I look at, but it’s one of the few things I can control, and it compounds in the background whether I pay attention or not.

A 0.03% vs 0.10% difference is not life-changing for most people. A 0.05% vs 0.75% difference absolutely can be, especially over 20–30 years.

Expense ratios are boring. They’re also one of the most reliable predictors of how much of the market’s return you actually get to keep.

Reference:

- SEC guide (definition of expense ratio): https://www.sec.gov/investor/pubs/sec-guide-to-mutual-funds.pdf

- Investor.gov on fund fees & prospectus fee table: https://www.investor.gov/introduction-investing/investing-basics/glossary/mutual-fund-fees-and-expenses

- ICI fee trends (2024 data; published March 2025): https://www.ici.org/files/2025/per31-01.pdf

If you want to understand the philosophy behind this site and how we approach ETF investing, you can learn more on our About page

Leave a Reply