I’ve gone down this rabbit hole more times than I’d like to admit. You start with a simple idea: “I just want one ETF that gives me the whole U.S. market.” Easy enough.

Entonces descubres que no hay solo uno. Hay varios. Y de repente estás comparando cosas como SCHB vs VTI, tratando de averiguar si uno es secretamente mejor que el otro.

Al principio, parece una decisión importante. Después de un tiempo, te das cuenta de que es principalmente una cuestión de preferencia.

Both SCHB and VTI are built to do the same job. They give you exposure to the entire U.S. stock market. You’re not trying to pick winners. You’re buying everything and letting the market do its thing over time.

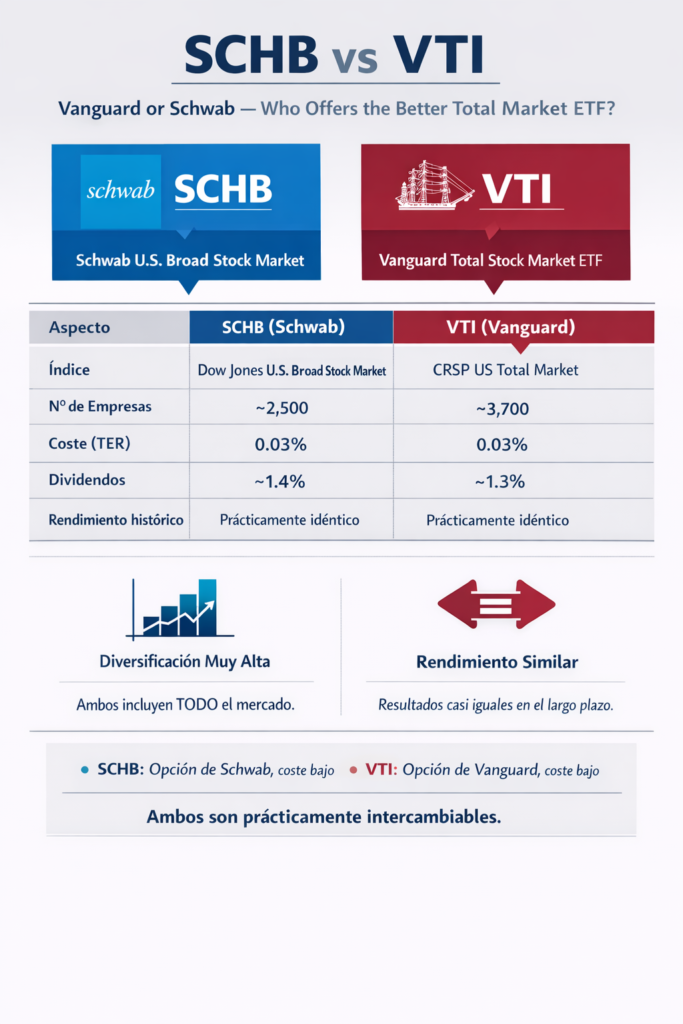

VTI, managed by Vanguard, tracks a very broad index that includes large, mid, and small-cap stocks. It holds more than 3,500 companies. SCHB, from Schwab, tracks a similar idea but with fewer holdings, usually around 2,500 companies. On paper, that sounds like a meaningful difference. In reality, it’s less dramatic than it looks.

The reason is simple. The U.S. stock market is heavily weighted toward large companies. The biggest names dominate both ETFs. So even though VTI includes more small-cap stocks, most of your money in both funds ends up in companies like Apple, Microsoft, Amazon, and Nvidia. That’s why their performance tends to look almost identical over time.

When it comes to cost, there’s basically nothing to separate them. Both charge an expense ratio of 0.03%. That’s about as low as it gets. For every $10,000 invested, you’re paying around $3 a year. It’s so small that it shouldn’t influence your decision at all. If you’re stuck on fees here, you’re focusing on the wrong variable.

Performance is where most people expect to find a clear winner. That doesn’t really happen. Over long periods, SCHB and VTI track each other very closely. Some years VTI comes out slightly ahead. Other times SCHB keeps pace almost perfectly. The differences are small enough that they don’t meaningfully change your long-term results.

The underlying reason is that both ETFs are capturing the same engine of growth: the U.S. economy. And more specifically, large-cap companies that drive most of the returns. Small caps are included, especially in VTI, but they don’t dominate the outcome.

There is one area where VTI has a subtle edge, and that’s structure. Vanguard has a well-known ETF structure that tends to be very tax efficient. Over long periods, that can reduce capital gains distributions in taxable accounts. It’s not something you’ll notice month to month, but over years it can make a difference.

SCHB is still tax efficient. It’s just that Vanguard has historically been particularly good at it. For someone investing through a tax-advantaged account, this probably doesn’t matter at all. But in a taxable portfolio, it’s one of the few real advantages VTI has.

Another difference people point out is size. VTI is massive. It manages hundreds of billions in assets and is one of the most traded ETFs in the world. SCHB is much smaller in comparison. That sounds important, but for most investors it doesn’t change anything. Both are highly liquid, easy to buy and sell, and widely available.

If anything, this is where the conversation starts to feel a bit forced. You can keep comparing details, but the conclusion doesn’t really change. These two ETFs are more alike than different.

At some point, I stopped trying to find the “better” one and started thinking in simpler terms. Where am I investing? What platform am I using? What feels easier to stick with?

If you’re already using Vanguard, VTI fits naturally. If you’re using Schwab, SCHB often integrates more smoothly, sometimes with commission-free trades or better compatibility with their platform. That kind of practical detail matters more than tiny differences in holdings.

The bigger risk isn’t picking SCHB over VTI or the other way around. It’s overthinking, delaying, or constantly switching between them trying to optimize something that barely moves the needle.

I’ve seen people spend weeks comparing ETFs like this and then invest nothing. Or they invest, then change their mind six months later, chasing a slightly better number. That behavior matters far more than which of these two you pick.

If I had to choose, I’d slightly lean toward VTI. Mostly because of its size, long track record, and that small edge in tax efficiency. But I wouldn’t hesitate to hold SCHB either. Not for a second.

In the end, both ETFs are doing exactly what you want from a total market fund. They give you broad exposure, low costs, and a simple way to stay invested over the long term.

That’s the whole point.

The difference between SCHB and VTI won’t make you rich. But sticking with one of them consistently just might.

This site was built to simplify ETF investing and remove the noise. You can read more about our approach and principles on the About page.

Leave a Reply